What is Financial Planning?

During my blogging hiatus, my life has encountered a few changes. One major change being that I'm now 2 months into my new job in - can you guess? - publishing! (See long story here & mid-way report here.) Having taken into account the state of starter salaries in the publishing industry (dismal), I've also kept my seasonal job. And if I may confess, although 6-day weeks have become typical for me, I still

During my blogging hiatus, my life has encountered a few changes. One major change being that I'm now 2 months into my new job in - can you guess? - publishing! (See long story here & mid-way report here.) Having taken into account the state of starter salaries in the publishing industry (dismal), I've also kept my seasonal job. And if I may confess, although 6-day weeks have become typical for me, I still occasionally quite often toy with the idea of quitting my part-time job. But that's a story for another day...

Last week, after 2 months of waiting for direct deposit, 401(k) and FSA deductions to be activated, I was finally able to figure out my cash flow and craft a simple spending plan. (Note: While I enjoy using Excel to better manipulate my data, I highly recommend YahooFinance's cash flow calculator.) I'm really excited to report that I'm currently saving 60% of my paycheck! Of course, that includes allotments for my new 401(k) plan, and House, Investment, and Savings funds.

One of my primary concerns in the last two years has been being my own financial planner. I found that my focus shifted as I went through various stages of employment. When I was working full-time, I focussed on:

- Goal setting: clarifying goals that are financial "biggies," e.g. buying a house, getting married, retiring

- Retirement planning: setting up & managing 401(k) & Roth IRA accounts

- Investment planning: for a non-retirement portfolio

- Investment review

Including: diversifying my portfolio, weighing the trimming of riskier stocks with acquiring "discounted" stocks - Insurance needs

A piece of advice from someone who decided to forgo this - health insurance is something everyone should have. If you ever find yourself without health insurance, pay for COBRA, sign up for HealthFirst. Do what you need to in order to be insured - it's worth the peace of mind of knowing you can get sick! - Funding future education

- Cash management: emergency fund, spending (including price shopping, impulse shopping, setting credit/cash/spending limits)

- Diversification: During the market flux, my networth moved in tandem with the erratic stock market - a sure sign that I needed to spread my eggs in different baskets!

- Estate planning: a will, a living will, power of attorney of healthcare

- Tax planning

As I continue to plod along in my quest to be an efficient financial planner for moi, I'm sure my priorities will continue to shift as well. Goals like buying a house will definitely open up worlds of concerns. But with the wealth of information available, I'm sure I'll be able to muddle through somehow. What concerns have you had as you moved through various stages of employment and life?

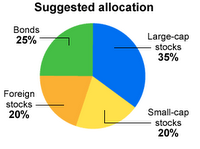

The guide suggests certain funds: the "Indexes," and funds with low expense rations (basically, funds labelled "Small-Cap Value" or "Large-Cap Growth"). And it also suggests using a

The guide suggests certain funds: the "Indexes," and funds with low expense rations (basically, funds labelled "Small-Cap Value" or "Large-Cap Growth"). And it also suggests using a